Income Streams

And everything that's wrong with them ...

In 1996, Bag scraped together a 25k deposit, took out a 30-year mortgage for the balance, and bought a home. To this day, it is the only Real Estate he has ever owned. Being a numbers guy, he ran some amortizations and calculated that an extra $86 per month on top of the mortgage payment would allow him to pay off the house in 15 years instead of 30. So he did it religously, eliminating 180 payments in the process, and the home was owned outright by 2011. A short time later, Bag was in the midst of starting a business, so he thought, why not go back to the same bank that held the original mortgage (JP Morgan Chase) and open up a 100k credit line on the house. He had little intention of actually using it, as he despises paying interest, but thought a credit line would be good to have as a backup plan, just in case.

So down to the local branch he went with his 800 credit score, the deed to his house, and a 15-year history with JP of making timely payments. The suits at the bank told Bag they could not open a credit line because the business he was starting was new and not yet generating sufficient income. To which Bag responded, True, but you are not loaning on the business - you are loaning against the house, which is worth at least double the 100k. They said, “Sorry, the house, the history, and the credit score are not enough - you need income to justify a loan.”

That experience was eye-opening. Bag walked out of the bank that day, shaking his head in disbelief and wondering how people in the business of loaning money could think like that. Seemingly, they were willing to loan long-term against (often temporary) income, as people change/lose jobs all the time. But bring them an asset that is a form of Permanent Capital (a house), and they don’t want anything to do with that. In hindsight, it’s hard to fault the suits at the bank for thinking that way. They are a product of their piss-poor education. Part of getting an MBA these days involves the completely, 180-degree, backward-ass idea that a proper business model for a bank is to borrow short & lend long. Where Bag comes from, that rational gets you knee-capped.

The faulty education that came with their MBAs is to blame for their frequently failing business model of loaning money long-term based on (often short-term) incomes. For whatever reason, the banks have never figured out that when those incomes are lost, and the loans can’t be repaid, they are left in the unenviable position of having to cry to the federal Government for help. Had the banks done the sensible thing and stuck to loaning short-term against assets they could foreclose on, aka Permanent long-term Capital, they wouldn’t need bailouts. While it might seem the HELOC Bag was trying get could have been a one-off isolated incident, it wasn’t. Even after the 2008 banking crisis and the bailouts that followed, Wall Street and the banks have not altered their thinking, one bit. They never learn. All they care about are income streams.

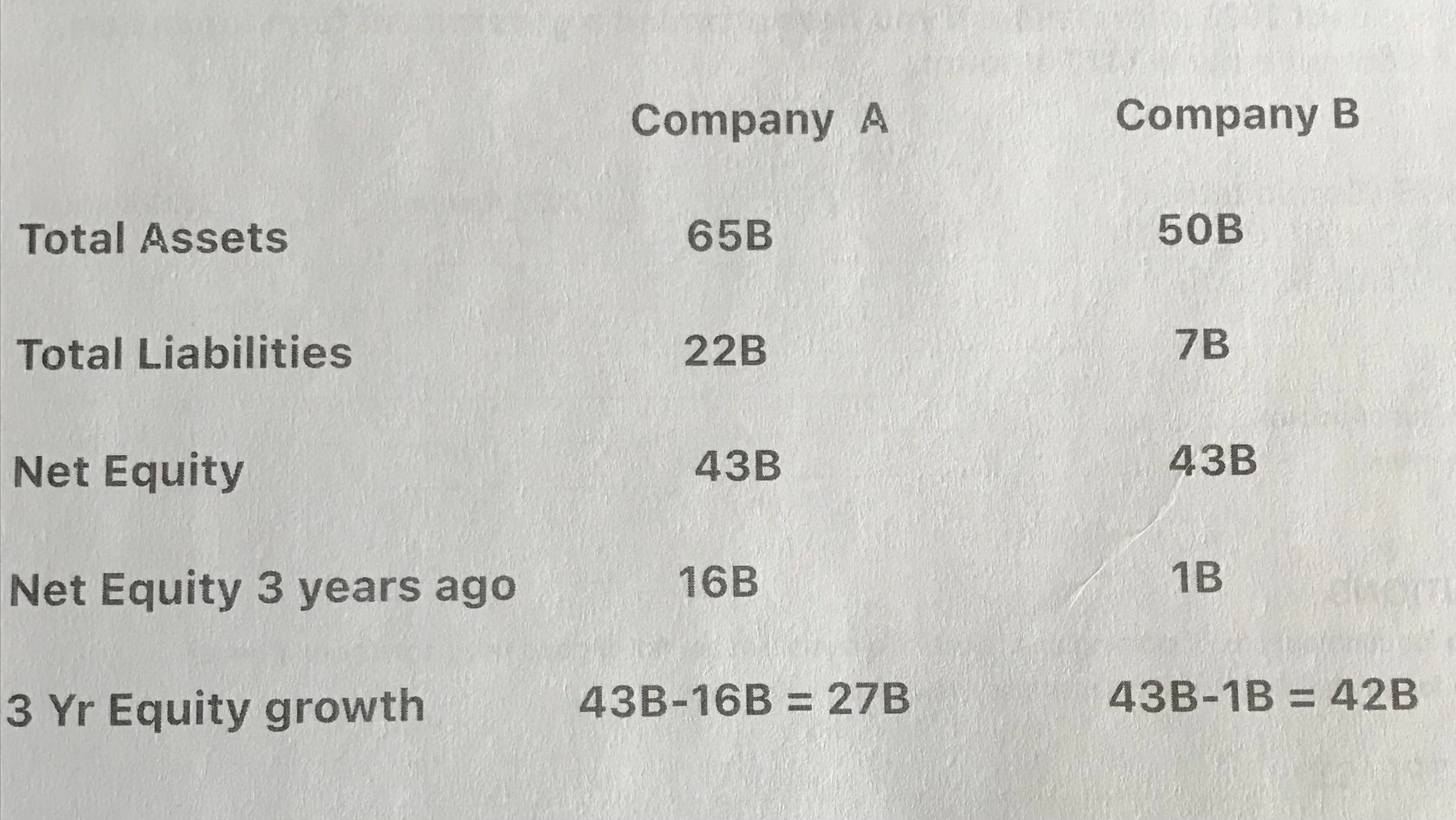

To further demonstrate this insanity, let’s consider two of the fastest-growing companies in the entire stock market. Company “A”, as of Dec 2024, had 65 billion in assets on their balance sheet and 22b in Liabilities for a NET Equity of 43 billion (65b -22b = 43b). The 43 billion is up sharply from 3 years ago when their net Equity was only 16 billion. Like we said, fast-growing.

Company “B” currently has 50 billion in assets with under 7 billion in liabilities, for a NET Equity of 43B, coincidentally equal to company A. Their 43 billion is also up sharply from 3 years ago when their NET Equity was under 1 billion. Like we said, even faster growing.

To summarize:

When comparing these two companies, there is one more thing worth considering. They both currently have a market share of more than 85% relative to their competitors in terms of the products they produce. According to multiple Wall Street analysts, company A's projected market share will fall to 50% in the next 5 years because they have no “moat” preventing a lengthy list of competitors from ramping up production. One of their chief competitors just opened up a 480-acre factory less than 15 minutes from Bag’s house. Company B, conversely, has a stellar moat with no such competition on the horizon. Consequently, their 85% market share is expected to grow in those same 5 years. Considering the moats (or lack thereof) and the data from the table above, one would expect company B to trade significantly higher than Company A. However, Wall Street, with their single-minded fixation on income and their complete inability to read a balance sheet, acknowledge moats, or recognize the faster growing company, has priced Company A at a premium to company B. In fact, in terms of Market Cap, A is currently priced at a mind-blowing 37 times the size of B. There is no world in which that makes sense.

For those who haven’t figured it out yet, company A is Nvidia. They are a 3.2 trillion dollar company that has added 27B in assets to their balance sheet in the last 3 years. Stated another way, Nvidia today is trading at a 74x premium to its net asset value (NAV). (3.2T / 43B = 74x). Any way you slice it, that is way spendy.

Company B is Microstrategy. They are an 85-Billion-dollar enterprise that has added 42B in assets to their balance sheet in the last 3 years. Stated another way, Microstrategy, compared to Nvidia, flaunts a microscopicly small 2x premium to their current net asset value (NAV). (86B / 43B = 2x). Any way you slice it, that is dirt-cheap.

How anyone in their right mind could justify Nvidia trading at 37x the market cap of Microstrategy is absolutely beyond Bag’s comprehension. It is even more insane when you compare the 74x NAV premium of Nvidia to the 2x NAV premium of Microstrategy. The latter is growing assets far faster, 42B in the last 3 years V. 27B, but trades at 1/37th the price for some reason. Either Nvidia is over-priced, Microstrategy is underpriced, or most likely, both. Bag would argue that it is inevitable that the market cap of these two companies will cross, as Microstrategy is the faster growth vehicle. Will they cross at 500 billion or 5 trillion? Bag is not sure, as both are plausible. Of course, Bag hopes it’s 5 trillion as it would make Microstrategy, which Bag is irresponsibly long, about a 60-bagger from here.

Bag knows there are plenty of Nvidia bulls reading this, and to you, he would ask:

Have you learned nothing from the Intel example of the late 90s???

Like Nvidia today, Intel was a Wall Street darling and the dominant chip maker in its day, sporting a ridiculous multiple, a near monopoly, and robust margins. But as Intel’s competition increased, those multiples and margins got compressed hard, turning Intel and their chip-making juggernaut into crumbs. Sure, Nvidia is making bank today. Their income statement is better than Microstategy’s by a mile. It might even continue that way for a year or two. But history teaches that thanks to competition, income for most companies, unless you keep innovating, is temporary at best. The Broadcoms, Taiwan semis, AMDs, and others are all storming the castle, and it is only a matter of time until Nvidia’s income, margins, and multiples get crushed as the market realizes there is no moat.

Income streams are grossly overrated when compared to the ability to grow assets. As evidenced by the last 3 years, Microstrategy is undeniably better at it than Nvidia. Until that changes, Bag will remain irresponsibly long Microstrategy.