Pick a commodity, any commodity …. Oil, Lumber, copper, cocoa, wheat, silver - you name it. What do you suppose happens to the price of that commodity if ONE entity could buy up the entire world’s production for, say, the next three years? In the world of economics, this is called “cornering” the market, and it is very rare. Free markets have two built-in mechanisms that prevent Corners from taking place. First, commodity producers will ramp up production to flood the market with more supply, making a “corner” more expensive and, thus, more difficult to achieve. Secondly, the price of the commodity itself will soar, which also, under normal circumstances, makes a corner more difficult.

Let’s consider a couple of historical examples. In the late 1800s, before John D. Rockefeller formed Standard Oil, a barrel of Oil - according to Google - was about 30 cents. At its peak, in the early 1900’s his company controlled about 80% of the US market, which was about 30% of world production. When the US government broke up Standard Oil, the price of a barrel of Oil was about $1.25 per barrel. So one entity, controlling less than a third of world production, managed to increase the price by more than 4x, making Rockefeller the wealthiest man on the planet in the process.

Another example of a near-corner in a commodity took place in Silver in the 1970s by the Hunt brothers. The descendants of an Oil tycoon decided that Silver at less than $2.00 per ounce was grossly underpriced. World Silver production at the time was just under 500 million ounces per year. So, at $2 per ounce, you could theoretically buy a year’s worth of production for about a billion dollars. Over the span of about five years in the 1970s, the Hunt Brothers threw about 2 billion dollars at the silver market - enough to purchase about two years of world production, or about 40% of world supply over those 5 years. The silver price responded by rising 25x to a peak of $50 in January of 1980.

So again, Bag asks what do you suppose happens to the price if ONE entity was able to buy up the ENTIRE world’s production of a commodity (not 30% like Standard Oil or 40% like the Hunt Brothers) …. I’m talking all of it!! Every crumb. Let’s further imagine a scenario where an increase in production of new supply of that commodity is physically impossible. With no new supply forthcoming, the only tool available to the market to prevent a corner, is a sharply rising price. As long as we are dreaming, let’s also imagine you have been gifted the opportunity to front-run the Entity looking to corner. Yes, it would be like buying silver at $2 before the Hunt brothers arrived or Oil at 30 cents before Rockefeller was piling in. This scenario is, quite literally, every investor’s wet dream. It just doesn’t seem like it could ever happen ….

Except….

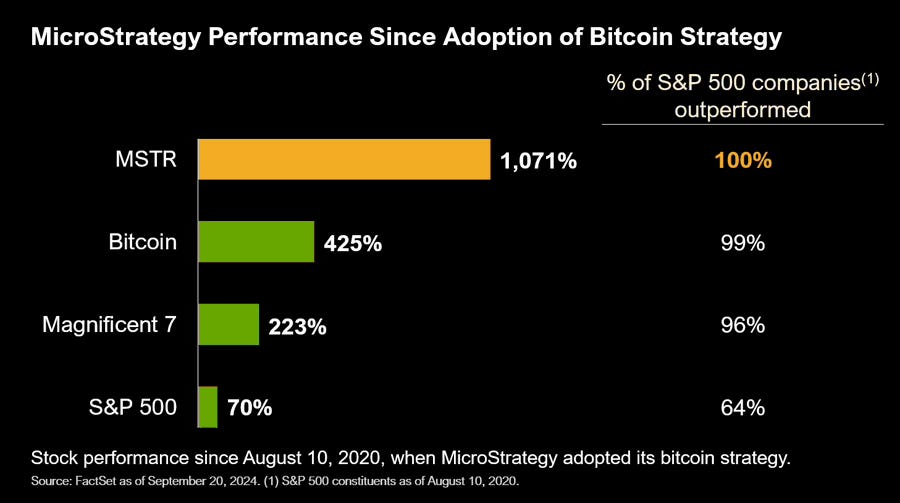

This past week, Microstrategy (trading symbol: MSTR) announced they will be raising 42 billion in capital over the next three years, nearly all of which will be immediately plowed into Bitcoin. Half of the $42B will be raised by selling new shares on the open market, the other half will be borrowed via bonds convertible into stock if the share price of MSTR rises. This is the biggest capital raise of any company in the history of the stock market!! Let that sink in. I repeat, the biggest capital raise in the history of Wall Street - and it’s not even close. The CEO of MSTR, Michael Saylor, whom Bag has written about before (link here) was kind enough to announce his plans, giving us all the opportunity to get into Bitcoin before he throws $42 billion at it. The current worldwide production of Bitcoin is 450 per day, with NO possibility of an increase. With a current price of about 69k, 450 coins (the daily issuance) could be bought for about $31 million dollars. The $42 billion Saylor plans to spend over the next three years amounts to over $38 million per day, more than enough to cover the $31 million dollar daily cost of what is being produced.

But wait, there’s more….

Instead of Front-running Saylor by buying Bitcoin, why not join him by buying Shares of MSTR? The real beauty of buying MSTR instead of Bitcoin is it provides leverage on your Bitcoin purchase. Bag apologizes in advance for the math that is about to follow, but it is necessary to understand exactly why MSTR will outperform Bitcoin. When you buy one Bitcoin, all you will ever have is one Bitcoin. Currently, when you buy one share of MSTR, you are buying .00107 Bitcoin. MSTR owns 252,000 BTC with 235,000,000 shares outstanding. 252k/235M = .00107 Bitcoin per share. Let’s shelve that for a moment.

Let’s make a few assumptions. First, Saylor is able to sell $21B worth of new shares at the current market price of $235 per share. Bag is of the opinion he will be getting more than the current $235, but let’s sandbag our estimate and assume it equates to 89,000,000 new shares (89M x $235 = $21B). The assumption that all those new shares won’t cause the stock price to fall will be further sandbagged by the fact that we will also assume that the Bitcoin price won’t rise despite all the buying pressure from MSTR. The assumption Bitcoin will not increase in price with all that buying is absurd, as the Oil & Silver examples above demonstrate. But let’s go with it for now … So, the proceeds from the sale of the 89M new shares at today’s BTC price of 69k will purchase 304,000 additional Bitcoin (304k x 69k = $21B) over the next 3 years.

Consider the $21B in Convertible bonds Saylor intends to sell. He has done six converts so far (link here) with an average interest rate of .635%. Yeah, we plebes get mortgages in the 7% range; this guy gets it at one-tenth the interest we pay. But I digress. That means the $21b in bonds will require $135m in yearly interest payments. If he plows 19B of the 21B from the bond sale into Bitcoin at 69k, it will fetch 275,000 additional Bitcoin. He can keep the other 2 billion on hand to fund his interest payments for the next 15 years. That way, he is never in a position (like the Hunt brothers) where he will have to sell assets (Bitcoin) to service his debt. Just like the prior six converts, the debt will not need to be repaid if the MSTR stock price rallies 50% above the current market - based on today’s price, that will be somewhere around $355. At that point, the bondholders can cash in their bonds for MSTR stock at a cost of $355, adding 59,000,000 shares (21B/$355) into the float.

Three years from now, there are only two possibilities:

MSTR & Bitcoin stay flat or go down in price….. MSTR will have the 235M shares that exist today + 89m shares from the Equity sale for a total of 324m shares outstanding. They will also owe $21B on their bonds, easily serviceable by the $2B held back. They will also have the 252,000 Bitcoin they have today + 304,000 from the equity sale + 275,000 from the converts, giving them 831,000 Bitcoin. Dividing the 831,000 BTC by the 324 million shares outstanding = .00256 Bitcoin per share. That is 2.4x your bitcoin, albeit with $21b in debt in only 3 years.

OR, MORE LIKELY …

MSTR & Bitcoin rally ….. which means they will have the 235M shares that exist today + 89m shares from the Equity sale + 59m from the converts for a total of 383,000,000 shares outstanding. They will have a pristine balance sheet with NO debt, and the 252,000 Bitcoin they have today + 304,000 from the equity sale + 275,000 from the converts, giving them 831,000 Bitcoin. Dividing 831,000 BTC by 383m shares = .00217 Bitcoin per share. In short, Saylor has more than doubled the Bitcoin per share (from the .00107 above to .00217) in only 3 years. That equates to a Bitcoin yield of 24% per year. The dude has invented the Wheel.

Rinse and Repeat ….

Bag can hear the whining now. Three years to double my money? That seems like a long time to be exposed to highly volatile assets like MSTR and BTC.

Well, let us consider the alternative. You could park some scratch in one of the Mag 7, for example, Apple. For the last 20 years, as a consumer, Bag has been an Apple guy. Apple iPod, Apple iPhone, Apple iPad, Imac, earbuds - you name it, Bag owns it. The products work right out of the box; they are intuitive, communicate seamlessly, and unlike Microsoft products - they do not constantly need to be rebooted & updated. Despite using their products for decades, Bag has never owned their stock. By almost any traditional metric used to evaluate a stock price, Apple has always appeared grossly over-priced. Today, for instance, the “trailing twelve months” (TTM) ending 9/30/2024 for Apple show gross sales of 385 Billion, with earnings of $6.09 per share. Those numbers are down from the 12 months ending 9/30/2023. In other words, their sales and profits are shrinking.

As of when this was written, Apple stock is trading at $225 per share with a price/earnings ratio of 37. So, when an investor buys a dollar’s worth of Apple stock, they are earning 2.7 cents per year on their dollar. This means that it will take 37 F*CKING YEARS for that one-dollar investment to earn another dollar. Now, this assumes they can maintain the current level of both sales AND profits for the next 37 years - (which they aren’t because, as we pointed out above, those numbers are shrinking). Can you imagine investing a dollar in a business today, which, if all goes well, will earn you a dollar 37 years from now? In the immortal words of Logan Roy … “Fuck Off.”

The idea of waiting a couple of generations to double your investment is precisely why Bag has never owned Apple stock, or any of the Mag 7, for that matter. If you think Bag is unfairly “Cherry” picking on Apple, consider this: Based solely on current earnings, The average (P/E) time to double your investment dollar in Microsoft, Amazon, Costco, Walmart, and Netflix is 42 years. These companies, on average, are earning 2-3% per year. Given the choice between earning 2-3% in one of those companies, or 24% more Bitcoin annualy in MSTR - let’s say it doesn’t take a degree in Finance to know where Bag is parking his money.

Interesting, I’ll have a look.

With Apple, if you got in back in 1986, you would have had a huge win. I did. Apple split multiple times and eventually started paying dividends. Back in the 80’s in tech it was customary to give shares as bonuses which at the time seemed like nothing, but shares in Apple, Sun Microsystems, Oracle, Intel eventually mattered and added up, so those bonuses ended up being huge. Also stock in many of those tech companies was relatively cheap so $1000 then netted a huge gain, which of course then you pay taxes but you never escape taxes…