Apple has been a Wall Street darling for decades. Anyone who bought AAPL stock when the iPod was sweeping across the nation in late 2001 and still has it today has made 700x their investment. Yeah, $1500 of AAPL stock then would be a milly today. The non-believers back then were granted *ahem* a second bite at the apple when the first iPhone was released in Jun 2007. Anyone who bought at that time has made 60 times their money. With seductive returns like that, it should be no surprise that many long-term holders of AAPL look at that stock with the same love and devotion as they do their own kids. In the eyes of long-term holders, AAPL can do no wrong. That is a dangerous mindset in the financial markets because it is rooted in emotion rather than logic. As with any stock, it is wise to let facts do the talking. This helps to better understand both the bear case and the bull case. We will explore both for AAPL today.

FINANCIALS:

Looking at the AAPL financials for the last three years, what really stands out is the fact that they have failed to grow revenues. Yeah, that’s right, their gross sales are shrinking. This is particularly egregious when considering the price inflation we have all experienced in the last few years. The prices for everything are rising, including Apple products, and yet AAPL cannot grow its top-line revenues, even with those higher prices. In terms of total sales, their best year was 2022, with 395M in revenue. AAPL closed 2022 with a stock price in the 120s. Today, on less revenue, they are inexplicably trading in the 240s. That gives them a price-to-earnings ratio of 38, more than double the S&P 500 average. Usually, a PE multiple of 38 is reserved strictly for the fastest-growing stocks in the index. While that may have applied to AAPL back in the day, it is clearly not the case now.

When discussing the outlook for AAPL stock with long-term bulls, the case they usually make is along the lines of: “Yeah, their revenues are down - but their earnings per share (EPS) is up - which means AAPL is becoming more efficient at wringing profit out of every dollar of sales.” As arguments go, it would be compelling if it weren’t so disingenuous.

When considering Earnings Per Share (EPS), there is a Numerator (Dollars earned) and a Denominator (# of shares). Changing either will alter the EPS output . Usually, the number of shares outstanding with most stocks tends to remain constant, thus requiring an increase in dollars earned to increase EPS. However, the shrewd accountants down at AAPL are aware that even a DECREASE in dollars earned can increase EPS provided the number of outstanding shares shrinks by a greater percentage than the dollars earned. For years now, AAPL has leveraged this gimmick by buying back shares of its stock, giving the appearance of stronger earnings when those earnings are, in fact, shrinking.

There was a time not too long ago when AAPL was the envy of the business world, sporting a corporate treasury with well over a hundred billion in cash and no debt. Not only have they burned through most of the hundred billion buying back shares, but they have also taken on over 100 billion in debt. With the debt side of their balance sheet growing, the days of providing a perpetual bid underneath their stock price and buying back stock to goose earnings are coming to an end. Stripping their corporate treasury of all that cash and replacing it with debt is a crystal clear indication that the suits running AAPL these days have no idea what to do with money and no vision for the future.

Further proof that they lack vision can be found in the Capital expenditures (CAPEX) number on their cash flow statement. CAPEX is the money corporations spend today to secure future revenue streams; think Amazon buying new trucks, Tesla opening a new factory, or Google building a new data center. The other tech behemoths (MSFT, GOOG, AMZN, and META) are spending, on average, 17% of their current revenues on CAPEX. AAPL is spending a little over 2%. Simply put, AAPL (unlike its competitors) is not finding creative use of CAPEX dollars to ensure future revenue; they are choosing instead to coast on momentum. Since CAPEX directly hits earnings dollar for dollar, minimizing CAPEX is a common accounting tactic corporations can use to maximise current earnings. Unfortunately for AAPL, with little CAPEX available to cut, they (unlike their competitors) will not have the option to rein in spending to goose earnings upward in the future.

INTANGIBLES:

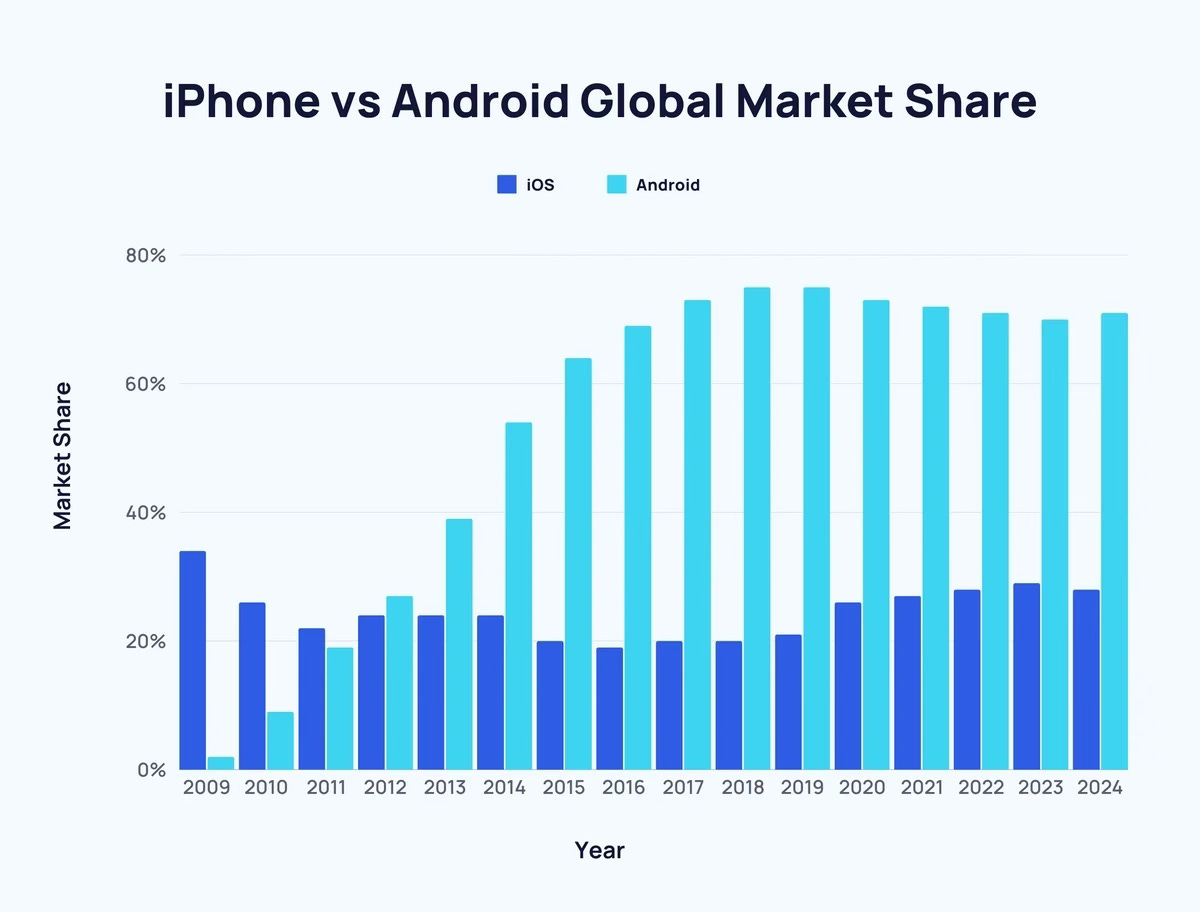

Bag’s three favorite non-financial metrics he likes to consider when evaluating potential stock investments are total addressable market (TAM), market share, and a moat. In other words, how big is the market they are chasing, what percentage do they own, and do they have a competitive advantage that keeps the competition at bay? Since the bulk of AAPL revenues comes from phones, let’s consider the phone market as it pertains to the three intangibles above. The TAM for smartphones is massive, no doubt. However, it is also heavily saturated, meaning the TAM is not growing much. Sure, there might be a few people running around Amazonian jungles who don’t already have smartphones, but that is about it. Since the phone market is not expanding, the real question becomes what is AAPL’s share, and is that growing?

As the chart above indicates, AAPL had 25% of the market 15 years ago; today, they have 27% - no real growth in 15 years. Over the same time frame, their chief competitor (Android) has grown from under 20% of the market to a current 68%. Bag would call that growth. As for a moat, Bag struggles to see it. Sure, they have their own operating system, which, in some ways, acts as a moat. However, it also acts as a barrier to expansion. If you are a developer creating the latest and greatest new app, would you do it for AAPL, which has 27% of the market, or Android, which has 68%? For this reason, far more apps are available on Android than on Apple, and it’s not even close. From a consumer point of view, this makes Android more appealing than Apple. It also goes a long way towards explaining AAPL’s inability to grow market share.

MACRO PSYCHOLOGY:

The way Bag sees it, AAPL is a giant ongoing psychological experiment for both the consumers of AAPL products (of which Bag is one) and those holding a position in AAPL stock (which Bag does not). Let’s start with the consumers. The latest iPhone Pro, with the big screen for us blind folk and a middling amount of memory, is over $1500 out the door + Apple care. There is a litany of competitors with phones costing a fraction of that. To their credit, AAPL has created an ecosystem where an iMac, iPad, iPhone, etc., all communicate seamlessly with one another. Buying a competitor’s phone means all that communication & convenience is lost. After having paid all this money to reap the benefits of a seamlessly communicating ecosystem, the consumer’s rationale is to bite the bullet and pay extra for the latest iPhone and keep it all going. This is a textbook example of what psychologists call the “sunk cost fallacy.” Kudos to AAPL for leveraging that particular psychological frailty.

The investors in AAPL are in a slightly different psychological cage. Decades of absurd returns have conditioned long-term holders to believe the stock price only goes up. It has left them emotionally attached; consequently, they dismiss bad news as something to be ignored. Sadly, they are living in complete denial of the facts laid out above. Namely, revenues are shrinking, profits are falling, cash is disappearing, debt is growing, their PE is double the S&P average, TAM is saturated, market share is not increasing, and while the other tech companies are spending CAPEX money on AI infrastructure - AAPL management is doing nothing to secure future revenues. Well, maybe it’s not nothing; AAPL did add an extra button on the side of the new iPhone 16. So, there is that.

The bottom line is that the bull case for owning AAPL at these levels has no merit. The bull arguments cannot withstand even the slightest scrutiny, as they are fraught with emotion and very little logic. The party in Apple stock the last 20 years has been magnificent, and understandably, the bulls do not want it to end. But the financials tell the tale, they are the proverbial turd in the punchbowl. If ever there was a time to look for the exit and find another party, it’s now. Bag is not alone in his thinking. You need go no further than the legendary Warren Buffet, arguably the greatest value investor of all time. If ever there was a guy who makes decisions on pure, unadulterated reason, without a shred of emotion, Warren is the guy. He has been raising cash by selling his Apple position at breakneck speed.

What Warren understands is this: AAPL’s current market cap is 3.6 trillion dollars, and they earned 95 billion last year. If you parked that same 3.6 trillion in US treasuries earning 4%, that equates to 145 billion per year in risk-free earnings. With no obvious path for AAPL to increase that 95 billion, it should not be a shock that Warren is choosing to pick up his share of the extra 50 billion in yearly earnings by sitting in treasuries. The fact that guy would prefer holding treasuries getting eaten by inflation rather than AAPL stock has to be frightening for long-term bulls. And yet, thanks to the power of denial, even Buffet’s selling won’t be enough to get the bulls to leave the party.

Excellent article. My favorite line, which must be in the top of the list in business strategy 101: Kudos to AAPL for leveraging that particular psychological frailty.

Great post and makes me question my long term holding… I’m mainly interested in services and their unfair cut they make on purchases. Anyway, this calls for a podcast in the near future. I got sick (again) so trying to get better and promised my friend to come on as a guest but you’re next in Que.